Multiple Logistic Regression is used to fit a model when the dependent variable is binary and there is more than one independent predictor variable. Before you proceed, I hope you have read our article on Single Variable Logistic Regression

Other concepts and data preparation steps we have covered so far are: Business Understanding, Data Understanding, Single Variable Logistic Regression, Training & Testing, Information Value & Weight of Evidence, Missing Value Imputation, Outlier Treatment, Visualization & Pattern Detection, and Variable Transformation

We will now build a multiple logistic regression model on the Development Dataset created in Development – Validation – Hold Out blog

Model Development

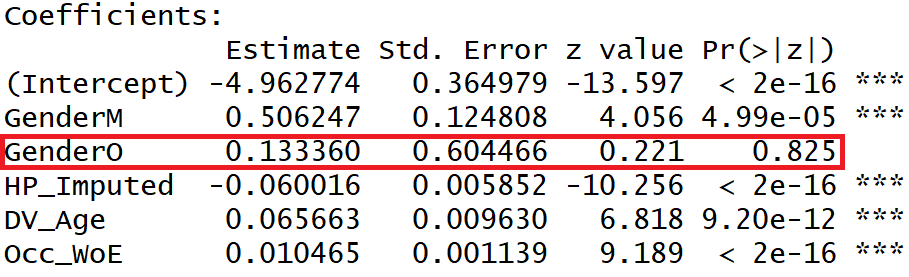

Let us build the Multiple Logistic Regression model considering the following independent variables and alpha significance level at 0.0001.

- Gender

- HP_Imputed

- DV_Age

- Occ_WoE

mylogit <- glm( formula = Target ~ Gender + HP_Imputed + DV_Age + Occ_WoE, data = dev, family = "binomial" ) summary(mylogit)

Interpretation of Model Summary Output

- We have set the alpha for variable significance at 0.0001. The p-value of the Gender variable is more than 0.0001 as such we may accept the Null Hypothesis, i.e. the Gender variable may be considered as insignificant and should be dropped.

- The beta coefficient of the independent variables is in line with their correlation trend with the dependent variable.

- HP_Imputed variable has a negative correlation with the Target phenomenon, hence it’s beta coefficient is negative,

- Whereas the other variables have a positive correlation and accordingly their beta coefficients have come positive.

Re-run after dropping Gender Variable

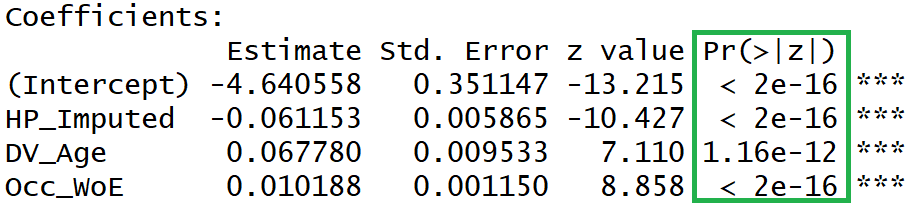

The Gender variable was insignificant in the above model run. As such, we drop the Gender variable and re-run the logistic function.

mylogit <- glm( formula = Target ~ HP_Imputed + DV_Age + Occ_WoE, data = dev, family = "binomial" ) summary(mylogit)

All the variables are now significant.

Predict Probabilities

# predict code in python dev["prob"] = mylogit.predict(dev) # predict code in R

dev$prob <- predict(mylogit, dev, type="response")

Model Performance Measurement

How good is our model? Is the model usable? Is the model a good fit?

To answer these questions we have to measure the model performance.

(I suggested reading our blog on 7 Important Model Performance Measures before executing the below code)

Rank Order, KS, Gains Table & Lift Chart

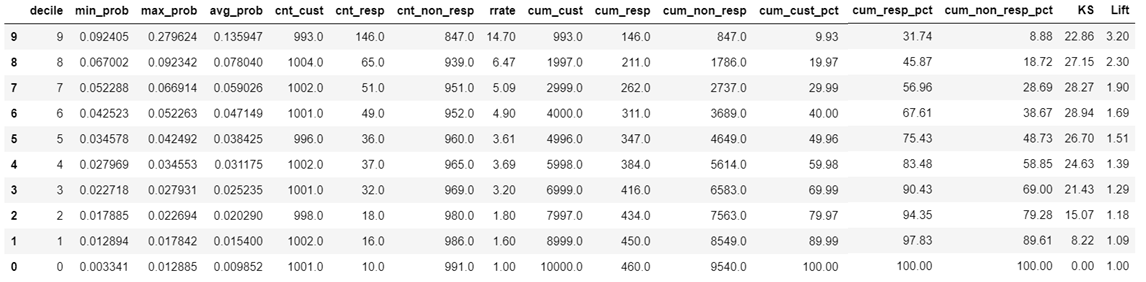

dev['decile']=pd.qcut(dev.prob, 10, labels=False) def Rank_Order(X,y,Target): Rank=X.groupby('decile').apply(lambda x: pd.Series([ np.min(x[y]), np.max(x[y]), np.mean(x[y]), np.size(x[y]), np.sum(x[Target]), np.size(x[Target][x[Target]==0]), ], index=(["min_prob","max_prob","avg_prob", "cnt_cust","cnt_resp","cnt_non_resp"]) )).reset_index() Rank=Rank.sort_values(by='decile',ascending=False) Rank["rrate"]=round(Rank["cnt_resp"]*100/Rank["cnt_cust"],2) Rank["cum_cust"]=np.cumsum(Rank["cnt_cust"]) Rank["cum_resp"]=np.cumsum(Rank["cnt_resp"]) Rank["cum_non_resp"]=np.cumsum(Rank["cnt_non_resp"]) Rank["cum_cust_pct"]=round(Rank["cum_cust"]*100/np.sum(Rank["cnt_cust"]),2) Rank["cum_resp_pct"]=round(Rank["cum_resp"]*100/np.sum(Rank["cnt_resp"]),2) Rank["cum_non_resp_pct"]=round( Rank["cum_non_resp"]*100/np.sum(Rank["cnt_non_resp"]),2) Rank["KS"] = round(Rank["cum_resp_pct"] - Rank["cum_non_resp_pct"],2) Rank["Lift"] = round(Rank["cum_resp_pct"] / Rank["cum_cust_pct"],2) Rank return(Rank) Gains_Table = Rank_Order(dev,"prob","Target") Gains_Table

Shown above is Gains Table output. The “rrate” (response rate) column shows that the model is Rank Ordering with a minor crack between decile number 5 & 4. The K-S statistic of the model is 0.2894 (28.94%). The Lift in the topmost decile is 3.20.

AUC-ROC

from sklearn.metrics import roc_curve

import matplotlib.pyplot as plt

%matplotlib inline

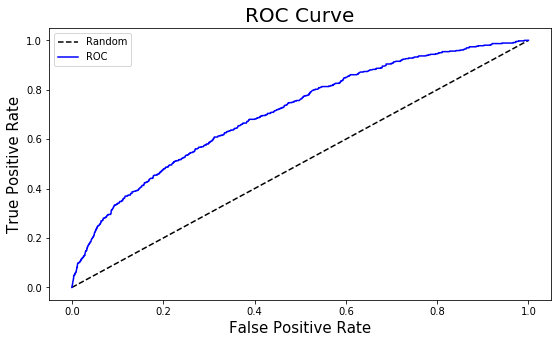

fpr, tpr, thresholds = roc_curve(dev["Target"],dev["prob"] )

plt.figure(figsize=(9,5))

plt.plot([0, 1], [0, 1], 'k--', label = 'Random')

plt.plot(fpr, tpr, color = 'blue', label = 'ROC')

plt.xlabel('False Positive Rate', fontsize=15)

plt.ylabel('True Positive Rate', fontsize=15)

plt.title('ROC Curve', fontsize=20)

plt.legend(fontsize=10, loc='best')

plt.show()

from sklearn.metrics import auc roc_auc = round(auc(fpr, tpr), 3) KS = round((tpr - fpr).max(), 3) print("AUC of the model is:", roc_auc) print("KS of the model is:", KS)

AUC of the model is: 0.707 KS of the model is: 0.297

The AUC of the model is 0.70. Based on AUC’s interpretation, the model may be considered to be a poor or just fair model.

Gini Coefficient

gini_coeff = 2 * roc_auc - 1

print("AUC of the model is:", roc_auc)

Gini Coefficient of the model is: 0.414

Hosmer-Lemeshow Goodness of Fit Test

#Hosmer-Lemeshow Goodness of Fit Function def chisq(data,groupby,obs,Exp):

chisq_tbl=data.groupby(groupby).apply(lambda x: pd.Series([

np.size(x[obs]),

np.size(x[Exp][x[Exp]==1]),

np.size(x[Exp][x[Exp]==0]),

np.sum(x[obs]), (np.sum(1-x[obs])) ], index=(["cnt", "Obs_Resp", "Obs_Non_resp", "Exp_Resp", "Exp_Non_Resp"]) )).reset_index() chisq_tbl=chisq_tbl.sort_values(by=groupby,ascending=False) chisq_value = ( ((chisq_tbl["Obs_Resp"]-chisq_tbl["Exp_Resp"])**2 /chisq_tbl["Exp_Resp"])+ ((chisq_tbl["Obs_Non_resp"]-chisq_tbl["Exp_Non_Resp"])**2 /chisq_tbl["Exp_Non_Resp"])).sum() g = len(data["decile"].value_counts()) chisq_tbl = chisq_tbl.round(0).astype(int) import scipy pvalue=scipy.stats.chi2.pdf(chisq_value , g-2) return({"Chisq_Table":chisq_tbl, "hosmerlem": {"degree_of_freedom": g-2, "X^2":round(chisq_value,2), "p_value":round(pvalue, 5)}})

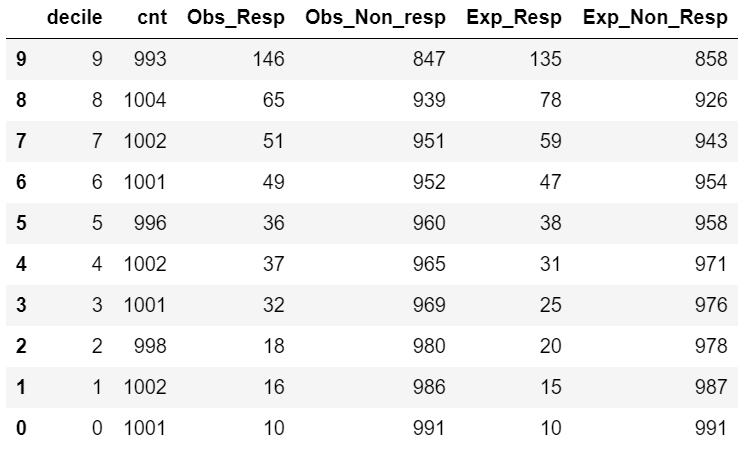

chisq_test = chisq(dev, "decile", "prob", "Target")

chisq_test["Chisq_Table"]

chisq_test["hosmerlem"]

{'degree_of_freedom': 8, 'X^2': 8.13, 'p_value': 0.09606}

The p-value of the HL-GOF test is above 0.05. We may accept the Null Hypothesis, i.e., the model fits the data very well.

Practice Exercise

- The KS, AUC, Gini Coefficient of the above model suggests that the model is just fair. It is not a very good model. Improving the above model is an exercise for the blog reader.

- Remember, in the above regression, we have not used the Balance, No. of Credit Transactions, and SCR variable. Try to bring these variables into the model and improve the overall model performance.

- We used the Occ_WoE variable in the above model, however, we could have used the Occ_Imputed or Occ_KNN_Imputed imputed variables as created in the Missing Value Imputation step.

<<< previous blog | next blog >>>

Logistic Regression blog series home

Recent Comments