In machine learning, we apply Variable Transformation to improve the fit of the regression model on the data. The functions such as Natural Log, Exponential, Square, Square-Root, Inverse, Binning/Bucketing, or some business logic is commonly used to perform variable transformation. In this blog, we will see how a simple variable transformation step can improve the model performance by about 10%.

Multiple Linear Regression Model

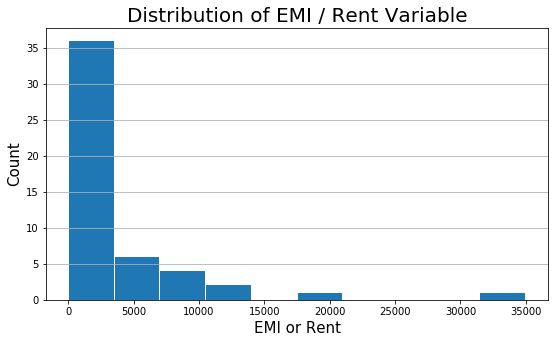

In the previous blog, we had built a multiple linear regression model using three variables, Mthly_HH_Income, No_of_Fly_Members, and Emi_or_Rent_Amt. The Adjusted R-Squared of the model is 0.678. Moreover, it was observed that there is skewness in the Emi_or_Rent_Amt variable. Shown below is the histogram plot of the Emi_or_Rent_Amt variable for quick remembrance.

plt.figure(figsize=(9,5)) plt.hist(inc_exp['Emi_or_Rent_Amt'], rwidth = 0.98) plt.title("Distribution of EMI / Rent Variable", fontsize=20) plt.xlabel('EMI or Rent', fontsize=15) plt.ylabel('Count', fontsize=15) plt.grid(axis='y')

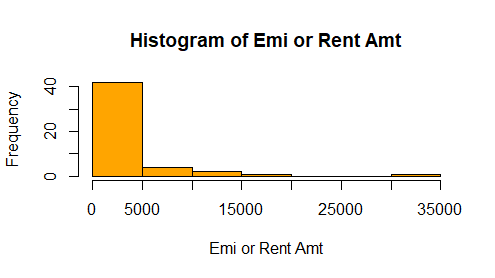

hist(x=inc_exp$Emi_or_Rent_Amt, main = "Histogram of Emi or Rent Amt", xlab = "Emi or Rent Amt", ylab = "Frequency", col = "orange")

Variable Transformation

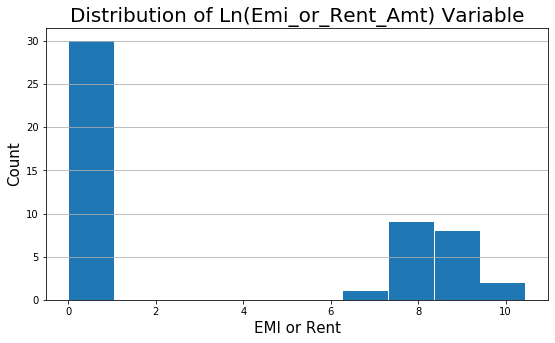

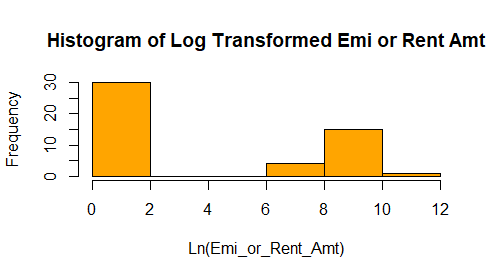

From histogram, we see there is skeness in the variable Emi_or_Rent_Amt. I propose we should do a Natural Log transformation of the variable. The log normal functions will scale the variable and make it somewhat normally distributed.

# Log Transformation step import numpy as np inc_exp['Ln_Emi_or_Rent_Amt'] = np.log(inc_exp['Emi_or_Rent_Amt'] + 1)

# Histogram plt.figure(figsize=(9,5)) plt.hist(inc_exp['Ln_Emi_or_Rent_Amt'], rwidth = 0.98) plt.title("Distribution of Ln(Emi_or_Rent_Amt) Variable", fontsize=20) plt.xlabel('Ln (Emi_or_Rent_Amt)', fontsize=15) plt.ylabel('Count', fontsize=15) plt.grid(axis='y')

inc_exp$Ln_Emi_or_Rent_Amt = log(inc_exp$Emi_or_Rent_Amt + 1) hist(x=inc_exp$Ln_Emi_or_Rent_Amt , main = "Histogram of Log Transformed Emi or Rent Amt", xlab = "Ln(Emi_or_Rent_Amt)", ylab = "Frequency", col = "orange")

Model Performance Comparison

We will compare the model built with & without variable transformation to see the improvement in Adjusted R-Squared model performance measure.

Note:

In linear regression, there is no assumption that the explanatory (independent) variable should be normally distributed. However, the model performance is improved significantly by transforming a skewed independent variable and making it normally distributed.

Related reading: Variable Transformation example in Logistic Regression Model

Practice Exercise

We have used only the initial 3 explanatory variables. The variables Highest_Qualified_Member & No_of_Earning_Member has been left as a practice exercise.

Next Blog

In the next blog, we will learn how to predict the estimated value, compute residuals (error), RMSE, and more.

<<< previous blog | next blog >>>

Linear Regression blog series home

Recent Comments